Let’s close the gender investment gap!

Oct 9, 2024

#Whoruntheworld?Girlswhoinvest!

Investing is a powerful way for building financial independence, yet a significant gender investment gap persists, with women investing far less than men. This disparity isn’t new – and we observe it as well within the neon user base – nor is it just about income differences; it’s deeply rooted in socio-cultural factors. In this blog, we’ll explore the reasons behind this gap, highlight the strengths women bring to investing, and provide actionable steps to help women confidently embark on their investment journeys. Let’s close this gap together!

At neon, we’ve always strived to create a platform that serves everyone equally. But when it comes to investing, we’ve noticed a significant gender gap that we need to address. While our overall user base is growing more balanced – now at 60% men and 40% women, a big improvement from our initial 85/15 split in 2018 – we see a similar disparity in our investment users. Today, only 22% of our actively investing users are women and the 78% remaining are men. This mirrors the broader investment world globally and in Switzerland, where women are less likely to invest than men. It’s time for us to explore the reasons behind this divide and, more importantly, to take collective action to close that gap.

Women and investing – why you should care

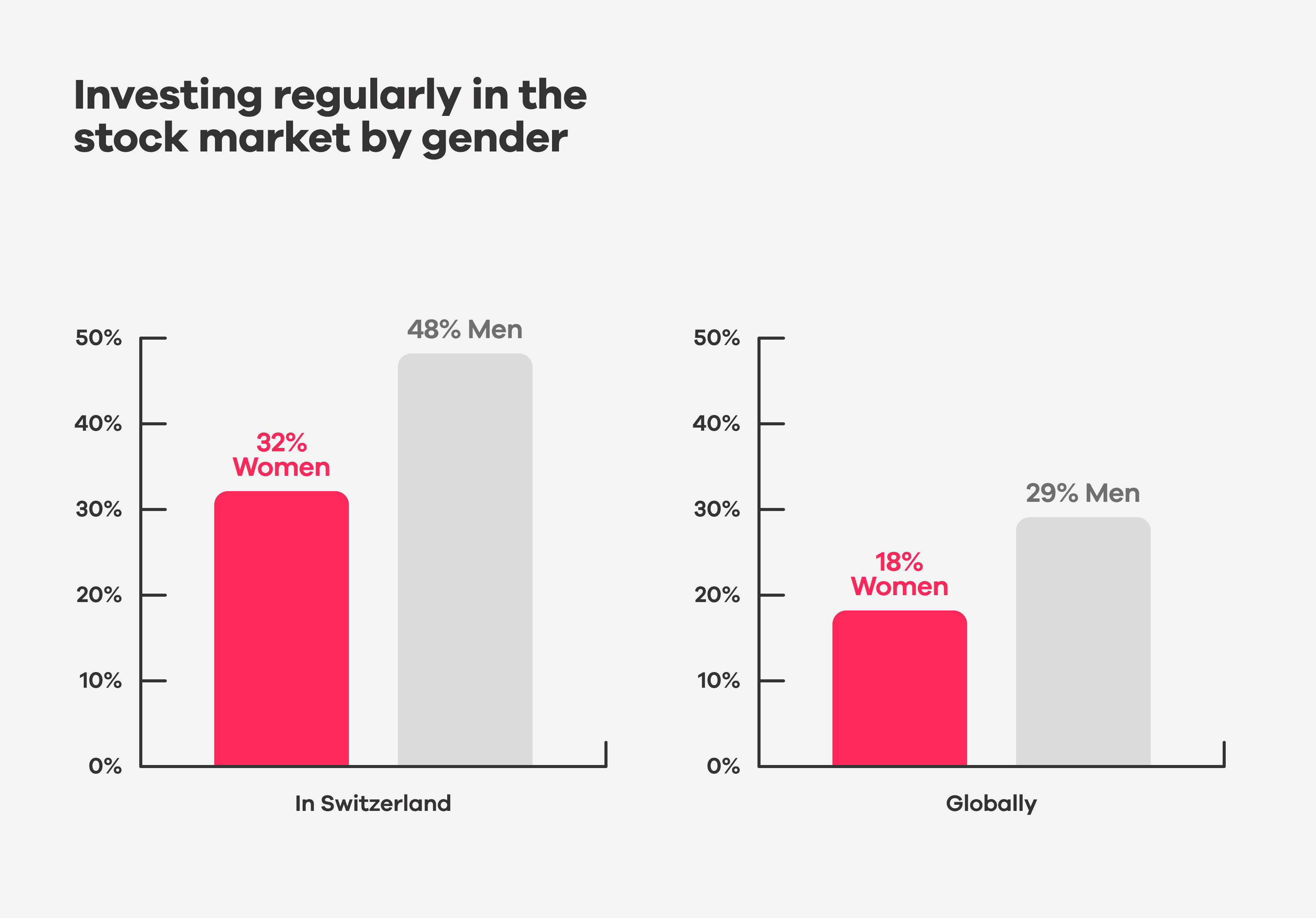

Globally, less than one in five women invest regularly compared to one third of men (JP Morgan). This difference is also visible in Switzerland: Only 32% of women invest a portion of their savings in shares or funds, compared to 48% of men. The issue at hand isn’t that women save less – 79% of women are able to put money aside on a regular basis – but they tend to have a more conservative approach to saving (Sotomo). More than half of women prefer the safety of a savings account rather than investing in the stock market (Sotomo, Gothaer). The fact that women invest significantly less than men is not just a result of financial inequalities, but also stems from deep-rooted socio-cultural factors. As a result, women miss out on wealth they could have gained by investing earlier and more. Let’s have a closer look!

Understand the 3 gaps: pay, pension and investment gaps

Gender Pay Gap

In Switzerland, there is still a significant income difference between men and women. The difference amounted to 9.5% in 2022 (Federal Statistical Office). This pay gap leads to further gaps, such as the pension and the investment gap.

Pension Gap

When women retire, the pay gap often becomes a pension gap, since a part of the pension depends on your salary and the number of years you have worked in the profession. The mothers among them who did reduce or even completely broke from the workforce will face its multiplying effect: An even bigger pension gap. 42% of women with children reported having years where they made no contributions to their occupational pension plans. Mothers are nearly twice as likely as fathers to have gaps in their pension contributions. As a consequence, women with children are disproportionately affected by the pension gap; only 38% of mothers say they have no gap in their pension provision, compared to 67% of men (Sotomo).

Investment Gap

Women often have less disposable income available for investing than men. Consequently, a significant number of women feel that they don’t have enough savings to invest in a meaningful way – about one third of women compared to only a quarter of men (Sotomo) – and they will keep on saving instead of investing. As a consequence, women also face the opportunity cost of not getting the compound interests that would have derived from their earlier and higher investment.

(Perceived) lack of financial knowledge

Women’s conservative approach to saving and investing is often linked to a perceived lack of financial knowledge. According to the Sotomo study, 36% of women rate their financial literacy as poor, while only 20% feel confident about it. In contrast, men tend to have a more positive self-assessment, with 33% viewing their financial knowledge as good.

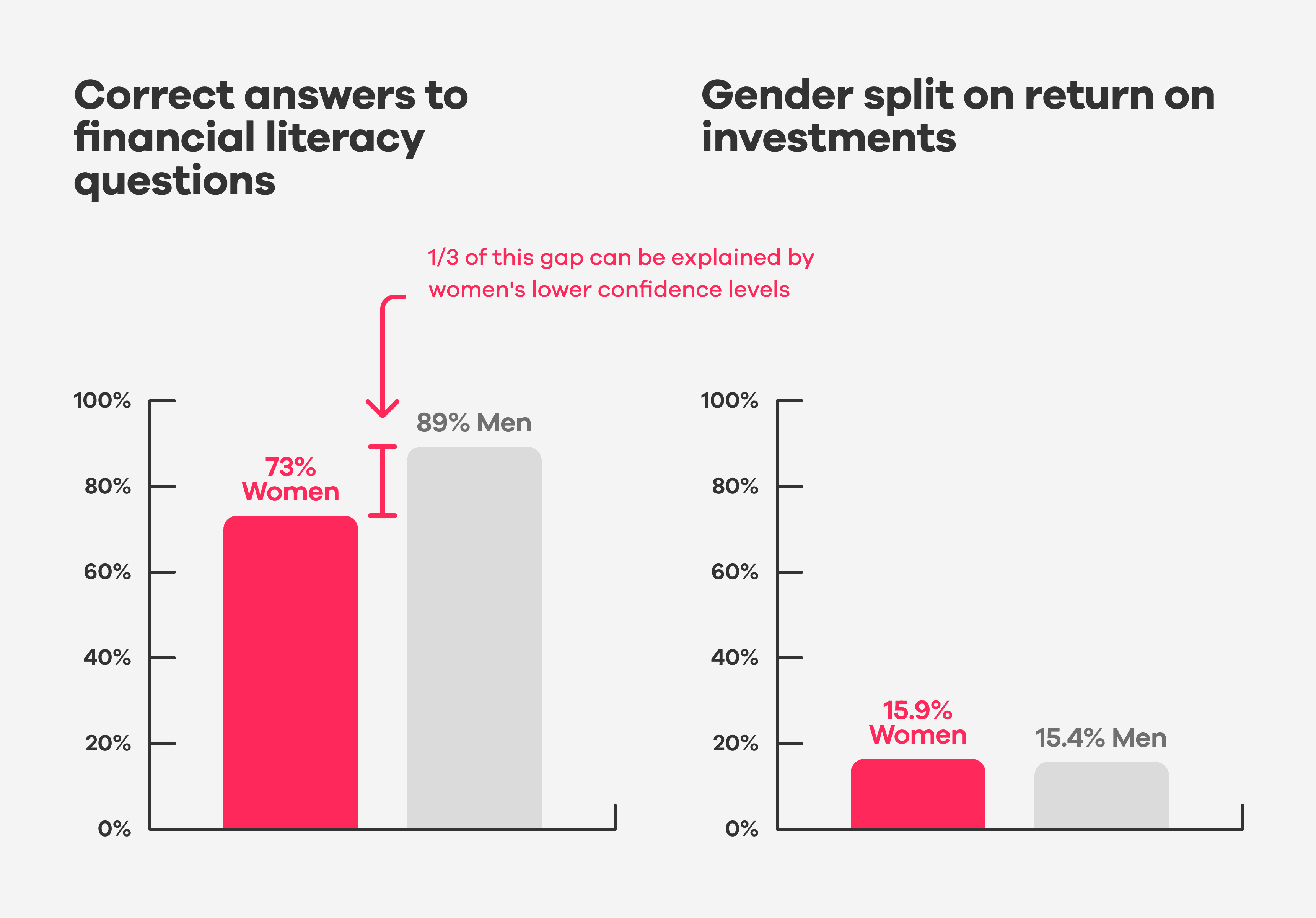

This self-assessment by women is only partially consistent with the objective survey of financial knowledge. There, 73% of women answered at least two of the standard «Big Three» financial literacy questions correctly, compared to 89% of men. According to a study by ZEW (Leibniz Center for European Economic Research) about one-third of this financial literacy gender gap can be explained by women’s lower confidence levels.

According to the Sotomo study, one major reason for this lack of financial knowledge and confidence is the traditional division of roles between partners. In Swiss households, it’s still more common for men to take charge of financial decisions and management tasks. Women, on the other hand, often focus more on household duties, organising daily tasks, childcare, and managing interpersonal matters. Even though it’s a hard truth to accept, the current situation is not surprising, since Swiss married women were not allowed to open their own bank accounts until 1988 if their husbands were not in agreement with it.

Making the financial industry more inclusive

The financial industry has traditionally been male-dominated, with marketing and communication strategies often geared more towards men. In fact, according to a study by BNY Mellon, nearly 9 in 10 asset managers (86%) acknowledge that their default investment customer is typically a man. Additionally, three-quarters of asset managers (73%) admit that their organisation’s investment products have historically been designed with men in mind (BNY Mellon). As a result, women often encounter financial products and services that feel less tailored to their needs, which can discourage them from engaging with financial institutions or exploring investment opportunities.

However, this dynamic is beginning to shift. Increasingly, financial institutions are launching campaigns and initiatives specifically aimed at addressing the unique financial challenges faced by women (we love to see it!). While there's still work to be done, these positive changes are helping make the financial industry more inclusive and welcoming for women investors. Read on to find out what happens when women actually do invest.

What happens when women do invest?

When women do invest, they tend to be more risk-averse. This (more) cautious approach often leads women to pursue a long-term investment strategy, which, while prudent, may limit the potential for higher returns that come with a more balanced risk strategy. However, this long-term perspective can also be a strength. Women who invest are often less fazed by the ups and downs of the stock market, staying committed to their investment goals even during periods of volatility (Axis mutual fund).

Women also tend to have a slightly better performance when they invest: In a direct comparison, women had 0.5% better portfolio performance than men in 2023 (ING study). They also tend to prioritise investments they can identify with, such as those with strong environmental, social, and governance (ESG) credentials.

You can be investing queens, smart and keen (if you’re above eighteen!)

These statistics are not just numbers; they represent real challenges that women face in achieving financial independence. But the good news is that these challenges are not insurmountable. With the right knowledge and tools, women can – and should – take control of their financial futures. So: it’s time to shift focus to what you can do about it. Here are 5 steps to start your investment journey.

5 Steps to Start Investing

Step 1: Determine your budget

Before you invest, you should know how much you can comfortably set aside each month. If you haven’t already, check out our budget blog and tool to help you get a clear picture of your finances. Knowing your budget will help you avoid overcommitting and ensure that you can sustainably commit to your investment goals in the long run.

Step 2: Write down your investment goals

Once you’ve figured out how much you can invest, it’s important to set clear investment goals. Are you aiming to save for retirement, a down payment on a house, or to build an emergency fund? Next, think about your risk tolerance. For example, if you prefer lower risk, many investors opt for broad ETFs, which offer diversification over the long term. If you're comfortable taking on more risk, you might explore other options like stocks that could offer higher potential returns. Your goals and comfort with risk will guide you on the best approach for your investment strategy.

If you prefer more guidance, we have partners who will help you navigate those questions through a robo-advisor – a service that uses computer algorithms to create and manage your investment portfolio automatically. Head over to the offers from our partners findependent or Selma.

Step 3: Decide on your assets

Once you've identified your goals, you need to choose the right types of investments to help you meet them and suit your risk tolerance. There’s quite a variety of options to choose from, from stocks to exchange-traded funds (ETFs). The golden rule is to diversify. When it comes to building your portfolio, make sure you diversify – or spread your risk – by investing in different asset classes. If you’re still thinking «WTF is an ETF?», then our «ABCD... ETF?» blog will navigate you through the most important terms of investing.

Once you’ve chosen the right asset for you, consider setting up an investment plan that automatically contributes to your portfolio once a month. By having your investments automated, you not only save mental energy, but also stay on track with your long-term savings goals (a classic win-win, that’s why we offer you an investment plan, read all about it here).

Step 4: Open an investment account

No investing without an investment account, that’s for sure. Make sure you check and compare the pricing and read the fine print before you open an investment account. We’ve done the hard work for you and created a comparison of Swiss investment accounts.

Step 5: Just. Do. It. And stay the course!

The hardest part of investing is often taking that first step. But remember, you don’t need to be an expert to start. Use the tools available to you and start small if you’re not very confident just yet. The key is to get started. Even if it’s just with 10 CHF to try out and see how the market behaves. Investing is a long-term commitment and consistency is key.

Let’s Close the Investment Gap together

Closing the gender investment gap isn’t about our percentage in our user base; it’s about empowering women to take control of their financial futures. At neon, we’re committed to providing the tools, resources, and support you need to confidently invest. It’s time to take that first step and start building the future you deserve. Let’s close this gap, together! ✊🏿✊🏻✊🏽

—

Useful resources at neon

Check out our how-to-videos:

Our favourite platforms and finance bloggers for women

Miss Finance by Angela Mygind

liebefinanzen.ch by Helga Bächler

corinnebrecher.com by Corinne Brecher

ellexx.com by Patrizia Laeri, Nadine Jürgensen, and Simone Züger

Madame moneypenny by Natascha Wegelin

Femmeinvest by Franscesca Barbera-Eckert

smartpurse by Jude Kelly and Olga Miler

herfirst100k by Tori Dunlap

Female Invest by Camilla Falkenberg, Emma Due Bitz, and Anna-Sophie Hartvigsen

Girlsthatinvest by Simran Kaur

Sources cited

«Frauen und Vorsorge – mehr Wissen für gleiche Chancen.» Sotomo, August 2022.

«Women and Investing. Planning for the Future.» JP Morgan, January 2021.

«Lohnunterschied: Erklärter und unerklärter Anteil des Lohnunterschieds zwischen Frauen und Männern.» Federal Statistics Office, March 2021.

«The Pathway to Inclusive Investing.» BNY Mellon, February 2022.

«Gothaer Anlegerstudie zeigt: Frauen investieren anders als Männer.» Gothaer, January 2023.

«Privatanleger-Analyse zeigt: Frauen auf dem Vormarsch.» ING, March 2024.

«Women investment behaviour report 2024: Insights into how women invest.» Axis mutual fund, February 2024.

«Fearless Woman: Financial Literacy and Stock Market Participation.» ZEW, March 2021.