What you need to know about the third pillar

Nov 17, 2025

Whether you are planning for retirement or hoping to buy a home someday, the pillar 3a offers many advantages. We have summarised the most important points about tied pension provision for you in this blog and explain how the 3-pillar system works in Switzerland.

Let's do a thought experiment: Imagine fast-forwarding a few decades in your life, as if you had a magical pocket watch. And voilà: You are over 65 years old and retired. This means, among other things, goodbye work. You have significantly more time, but your monthly salary is also gone. In order for you to continue living comfortably at home, travel to distant countries, and generally enjoy life, there is the old-age provision – in Switzerland, this consists of three pillars.

The first and second pillars as the foundation of your provision

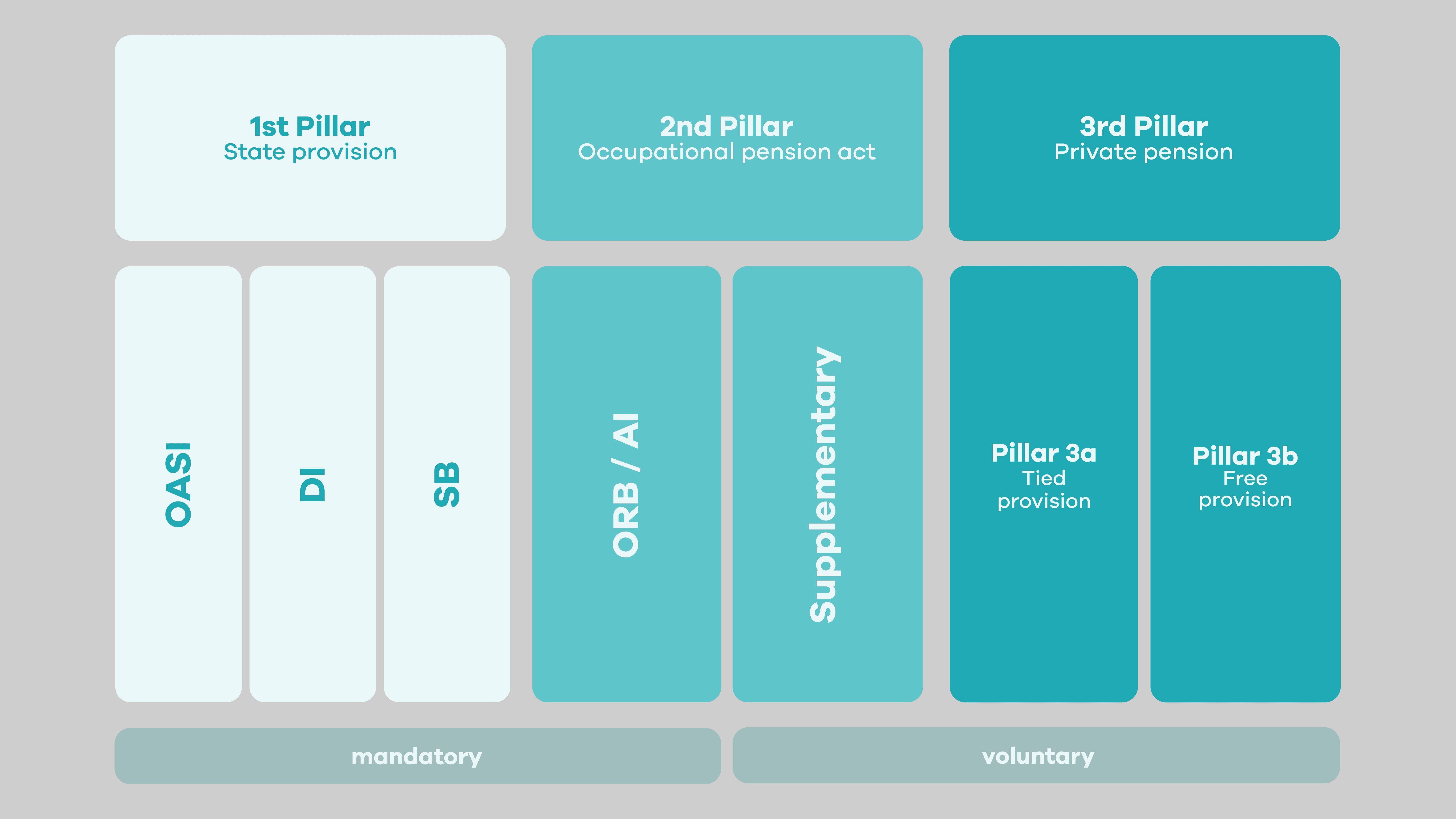

Before we get to the third pillar, it is worth taking a look at the first two pillars. They form the foundation of your old-age provision, but are often not enough to secure your lifestyle on their own.

1st pillar: state provision

The 1st pillar includes the old-age and survivors' insurance (AHV/IV in German, OASI/DI in English) as well as the so-called supplementary benefits (EL). It secures the existence of insured persons in old age, in case of disability, or in the event of death. Supplementary benefits step in when other state benefits or one's own income are not sufficient.

In short: Anyone who lives or works in Switzerland is automatically insured. The 1st pillar covers the essentials, but is not sufficient to maintain the accustomed standard of living.

2nd pillar: occupational provision

The 2nd pillar forms the occupational provision (BVG in German, ORB in English), often simply called «pension fund». It complements the benefits of the 1st pillar and ensures that you can continue your accustomed lifestyle in old age or in the event of disability. In the event of death, it also provides financial support to your dependents.

All employees with an income over 22'680 CHF (valid amount for 2025) are automatically insured through the pension fund. Self-employed individuals can also voluntarily join a pension fund. Therefore, the 2nd pillar, like the 1st pillar, is mandatory, but extends the coverage as another level for your financial safety net in old age.

Good reasons for a third pillar

You might now be asking yourself: Why do I still need a third pillar? Well, because when you're retired, the first two pillars usually cover only about 60% of your accustomed salary. And if you want to retire before 65, this percentage is even lower.

The voluntary third pillar closes this gap. It is divided into pillar 3a and pillar 3b:

Pillar 3a: tied pension provision

Pillar 3a primarily serves as old-age provision and is promoted by the Confederation through tax incentives. Contributions are possible up to a predetermined maximum amount and can be deducted from your taxable income. Furthermore, the accumulated pillar 3a assets are exempt from the wealth tax. Your money remains tied until retirement, hence the name «tied pension provision». In certain exceptions, you can access it earlier, more on that later in this blog.

Pillar 3b: flexible pension provision

Pillar 3b offers more flexibility and complements pillar 3a. You can invest the money in various forms, for example, in a savings account, in funds, shares, or in ETFs. Since there are no annual maximum contributions or contract terms, you have more flexibility, but the contributed amounts are not exempt from tax.

With neon invest, you can easily and affordably cover flexible pension provision, whether you want to save some extra for private projects or supplement your old-age provision. You can invest in shares or ETFs yourself, use investment plans to invest automatically on a monthly basis, or use our templates – our ready-to-use savings plans that make it easier for you to get started with investing.

How much you can contribute and when

Assuming we have piqued your interest and you want to regularly contribute to the third pillar in the future – like 62 percent of Swiss people between 25 and 64 years of age do. Then the rule applies: You can contribute from the age of 18 and up to the official retirement age or even five years longer if you continue working. There is also a maximum amount per year: for 2025, this is 7'258 CHF for employees. Self-employed persons and employees without a pension fund can contribute 20% of their income (up to an annual maximum of 36'288 CHF).

In which cases can you withdraw your money?

The money in pillar 3a is tied and cannot be withdrawn at will. The most common option is to withdraw it upon retirement.

Under certain conditions, it is possible to withdraw your 3a money early. This is possible if:

you buy a house or apartment,

you become self-employed,

you move your residence abroad,

you become disabled,

you transfer your 3a assets to a pension fund.

In the event of death, your 3a assets go to contractually designated beneficiaries, such as your partner or your children.

Patience leads to success

Your money for pillar 3a can be invested differently with most providers, from the classic savings account to funds. In a savings account, your money is held in cash, i.e., not invested. In funds, however, it is actually invested. The most common option is investing in funds, because this way you achieve returns on your invested money – in other words: your money works for you.

After a few years, this becomes particularly noticeable through the compound interest effect. Simply put: Your invested money earns interest, which in turn earns interest itself – almost like money making more money for you. Long-term investing also balances the volatility of the funds, i.e., the ups and downs of the markets. Therefore, it pays to start early and not constantly change the investment strategy. Instead, give your money time to work for you.

Paying retroactively into pillar 3a for past years

Finally, there is another important change regarding the third pillar, namely the possibility of retroactively paying into pillar 3a. As of January 2026, it will be possible to pay retroactively for up to ten years into pillar 3a and deduct it for tax purposes. Of course, this will also be possible with us.

However, there are a few things to keep in mind:

The 10-year calculation starts only from 2026. In other words: In 2026, you can pay retroactively for 2025 and in 2035 you can also pay for 2025.

The retroactive payment is only possible if the maximum amount for the current year has already been fully utilised.

Once you have started to withdraw your 3a assets, a retroactive payment is no longer possible.

If you have reached the official retirement age but have not yet withdrawn anything from your 3a account, a retroactive payment is still possible up to five years after retirement age.

If you want to know more about this, we recommend this page of the Confederation. There you will find the exact wording of the legal provision and more information.

The neon pillar 3a

There are many providers for a pillar 3a, and they all claim to be the best in their own way. We are, of course, quite convinced of our 3a offer as well. And as always, we don't want to promise you the world, but instead clearly and transparently present our prices and conditions. This is why you can read more about our 3a offer and how it compares to other providers in this blog.