Build wealth with the investment plan

With the neon investment plan, wealth accumulation is easy. You select up to six shares or ETFs and set the amount you want to invest each month. Then you can sit back and relax, because we take care of the rest – we automatically invest for you once a month. All at the usual low costs.

What is the investment plan?

With the investment plan, you select up to six shares or ETFs from the neon invest universe and specify the amount you want to invest each month. Then you can sit back and relax, because we take care of the rest – we automatically invest for you. And because we have no custody fees and low trading fees, you can save money in the long term with low monthly costs. So it's just as worthwhile for small investors as it is for high earners.

A brief digression #1: Why is the investment plan worthwhile?

You're thinking: I could simply invest in six shares or ETFs of my choice every month with neon invest, what's the point of the investment plan? Absolutely, you could. But with the investment plan, we make it easier than easy for you: on the one hand, you save valuable brain cells because you no longer have to worry about it once you've made a smart decision. On the other hand, you can use it to pursue your savings goals in the long term: Thanks to automation, you don't forget to invest every month. Classic neon: win-win.

The investment plan also helps you avoid trying to find the perfect time to invest − the so-called «market timing». Market timing is the strategy of anticipating market lows and highs in order to buy and sell shares or ETFs at the best possible prices.

Sounds tempting in theory, but doesn't hold up in practice: various studies show that it is almost impossible to correctly predict market developments and choose the perfect time to buy or sell investments*. Market timing can also lead to higher costs − for example due to missed opportunities, also known as opportunity costs. Investors often sell too early and buy too late. As a result, they miss out on the best days on the stock market. In addition, the constant buying and selling of investments can increase transaction costs, which reduces the return on your investments.

A better strategy is to buy shares or ETFs regularly over a certain period of time (like with our investment plan). This allows you to benefit from the cost-average effect, which means that you achieve an average entry price. In simple terms: you buy shares regularly, regardless of whether the price is currently high or low. This means that fewer units are bought over a longer period of time when the price is high and correspondingly more when it is low.

A brief digression #2: The investment plan vs. pillar 3a

Let's take a look at the investment plan in comparison with pillar 3a: Admittedly, the investment plan doesn't offer you the sexy tax deduction that pillar 3a does, but it does offer you more flexibility: because, unlike pillar 3a, you don't have a holding period with the investment plan, you can therefore withdraw as much money as you want at any given time. And you also determine the right time to sell your shares or ETFs in the future. With pillar 3a, you can withdraw your savings at the earliest five years before retirement − and then you have to withdraw everything at once (keyword: taxes!).

This is not a plea against pillar 3a, on the contrary. If you have the financial means, the best way to save is with pillar 3a and an investment plan. The investment plan simply offers you more flexibility. To put it in pop psychology terms: the investment plan is more for people with a responsible profile, but with slight commitment issues.

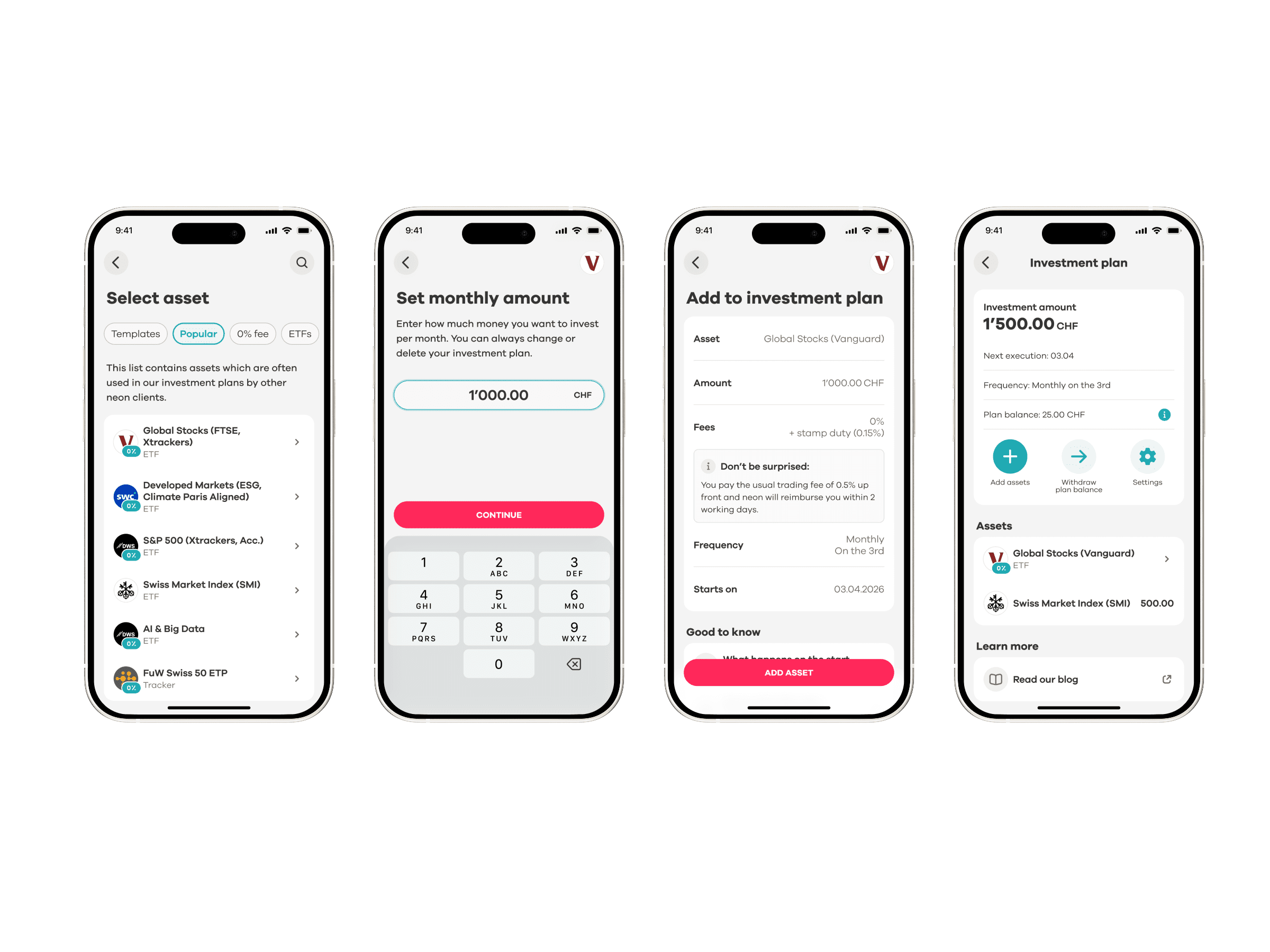

Where to find the investment plan and how to create one

To set up a investment plan, click on the «Invest» tab in the neon app and scroll down a bit until you see the investment plan. Click on «Start saving». Then select a share or ETF and the monthly amount you want to invest. Click on «Confirm» and the investment plan is set up.

It's just as easy if you want to cancel the investment plan: in the investment plan overview, click on the investment you want to change and then on «Delete». You can do this at any time, except on the day the investment plan is executed − then we will automatically invest in the shares or ETFs you have selected.

What the investment plan costs you

You can set up investment plans at no extra cost. And we don't charge any custody fees for your portfolio anyway. The only thing you pay are the trading fees: For Swiss shares and all ETFs it is 0.5% of the buy or sell price per transaction, for international shares the fee is 1% (there are no additional fees for currency exchange).

0% fees investment plan ETFs

As you have probably noticed so far: With the investment plan, we try to make your wealth accumulation as simple and favourable as possible. And there's one more thing on top: with the investment plan, you don't pay a trading fee when you buy selected assets. |

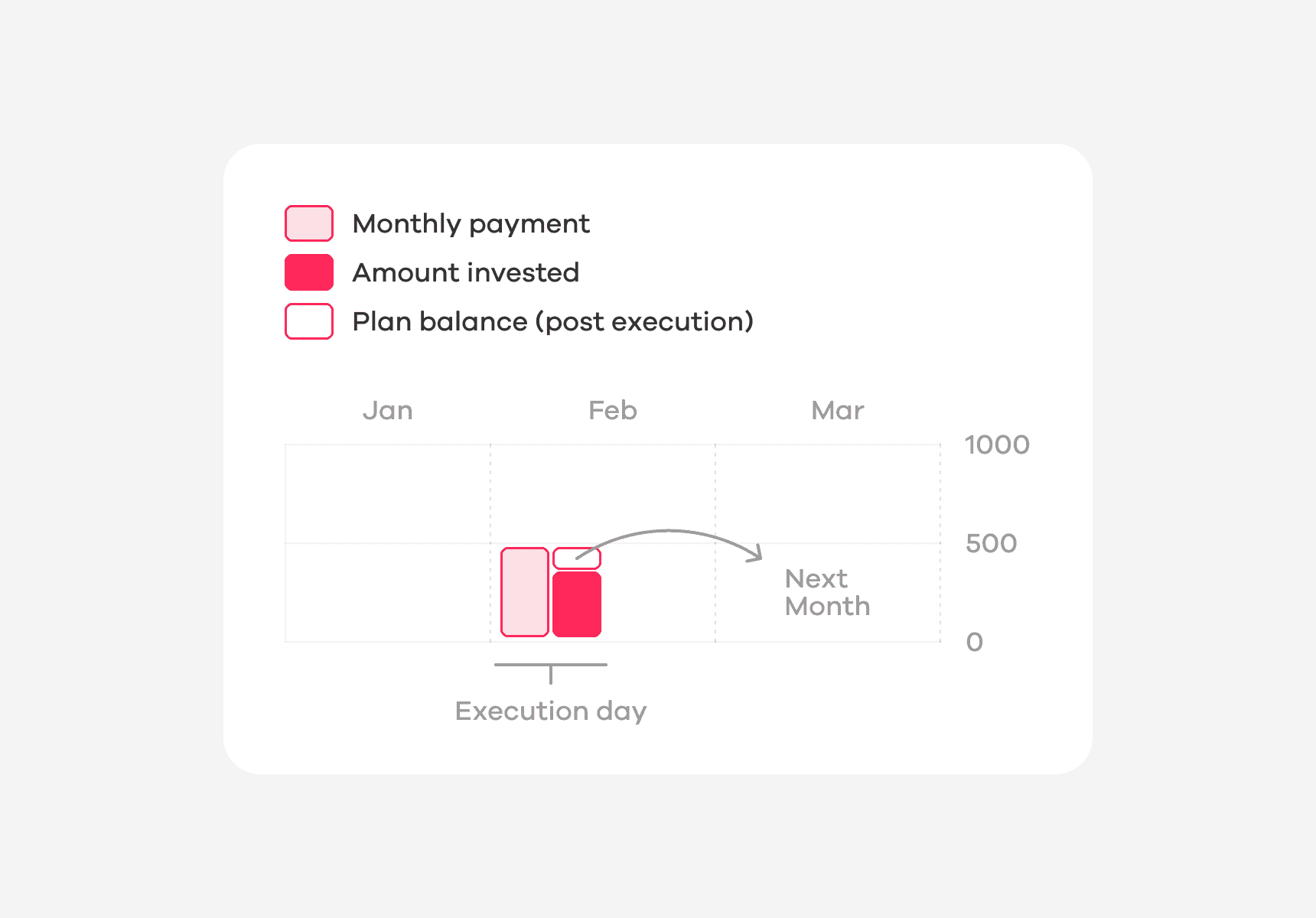

How the investment plan works in detail

You have resolved to put a total of 500 CHF aside each month. You decide to invest all of it in Apple. You set up the investment plan accordingly in the app. On the first day of the following month, your 500 CHF will be automatically invested in Apple. (Please note: This example is not a recommendation to buy Apple shares − we simply want to explain how the investment plan works).

As we always buy whole shares or ETFs, as many units (including fees) as possible are bought from your monthly savings. In your case, this means that 3 Apple shares are bought (price per unit 159.75 CHF** plus fees). This leaves a residual amount of around 20 CHF in the investment plan, which you can see under «Plan balance» in the investment plan overview. This amount will then be invested the following month in addition to the 500 CHF. If you want to use the plan balance for other purposes in the meantime, you can also have it paid out to your main account at any time.

How it works with multiple assets

The same principle applies if you want to invest in several assets. Let's take the same example: you want to save 500 CHF per month – you now invest 420 CHF in Apple and 80 CHF in the ETF Global Stocks (FTSE). Since, as mentioned above, we always buy whole shares or ETFs, as many units as possible (including fees) are purchased from your monthly savings.

Let's do the maths: 2 Apple shares are purchased with the 420 CHF (price per unit 204.95 CHF** plus fees). So a little less than 10 CHF remains, which goes into the Apple pot and is invested in Apple next month in addition to the 420 CHF. Exactly the same applies to the Global Stocks ETF: you can use 80 CHF to buy 12 units of the ETF (price per unit 6.20 CHF** plus fees). About CHF 5 remains, which will be invested next month in addition to the 80 CHF.

This means that even with several assets in the investment plan, there may be a remaining amount that you see under «Plan balance» in the investment plan overview. Think of it like this: there is a pot in the background for each investment that is replenished monthly and is reserved only for that particular asset. So in this example, there is one pot for Apple and one pot for the Global Stocks ETF. Please note: to make it clearer, you only see one «Plan balance» in the app itself, which combines both pots.

For further questions and answers, there is a separate FAQ category for the investment plan.

*Sources:

Brian J. Bloock: Market Timing Fails as a Money Maker in Investopedia 2024

Simon Moore: Busting the Myth of Market Timing in Forbes 2016

Hubert Dichtl, Wolfgang Drobetz, Lawrence Kryzanowski: Timing the Stock Market: Does it really make no sense? in Journal of Behavioral and Experimental Finance 2016

**Reference date for share and ETF prices and fees: 25.11.2024